|

The Week Ahead: Highlights

Asia-Pacific Preview

China Industrial Production, Retail Sales Up Next

By Brian Jackson, Econoday Economist

Chinese monthly activity data will be the main focus in the

Asia-Pacific region. Quarterly GDP data published last month showed a solid

start to the year but that largely pre-dated the impact of the Iran conflict.

Official PMI survey data for April at the start of the month showed weaker

conditions in both the manufacturing and non-manufacturing sector, while

inflation data earlier this week showed the biggest increase in producer prices

since 2022. This suggests next week's data will indicate some weakness in

conditions, which may prompt some commentary on the outlook in the accompanying

statement. The monthly review of the loan prime rate will likely extend the

period of stability seen over the last twelve months.

Australian labour market data for April will also be watched

closely for any impact from the Iran conflict. March data showed conditions

were steady and tight but officials at the Reserve Bank Australia earlier this

month noted anecdotal reports that hiring intentions had softened. This month's

NAB Business Survey also indicated weaker employment in April. Also out next

week will be the Westpac consumer confidence survey, which is likely show

sentiment remains impacted by both the Iran conflict and recent RBA rate hikes.

Singapore trade data for April follows another month very

strong export growth reported for March, with export growth supported by

ongoing demand for AI-technology and semiconductors. Singapore PMI survey data

earlier in the month also showed little impact from the Iran conflict on

conditions. New Zealand will also report monthly trade data and quarterly

producer price data next week. Hong Kong inflation data will likely show steady

price pressures, while the flash PMI survey for India will provide an early

indication of conditions in May.

Europe Preview

Watching for Mideast Effects

By Marco Babic, Econoday Economist

While the coming week is a relatively calm one for European

indicators, those slated for release will be closely watched to further gauge

the fallout from the conflict in the Middle East.

Most closely watched will be Germany's Ifo Business Climate

Index and GDP reports on Friday. The Ifo report for May will likely show

further deterioration in business sentiment which fell to a reading of 84.4 in

April, while business expectations dropped to 83.3 from 85.9.

Preliminary GDP estimates for Europe's largest economy have

a 0.3 percent gain for both quarterly and year-on-year results. The risk is

that with more information, the flash estimate will be revised lower. There has

been nothing to suggest in additional first quarter data that there has been

any improvement.

Also up in the week ahead are PMI reports for Germany, and

France which are likely to show further divergence between the manufacturing

and services economy. Last month saw increased activity for manufacturing as

businesses have been rushing to get orders in to get ahead of further price

increases and expectations for supply chain bottle necks. This in turn has made

producers more optimistic and leading to ramping up production.

This is, however, far from a virtuous cycle. While the

increased production is no doubt welcome, it could later lead to bloated

inventories should demand wane which it could do for a variety of reasons.

Among them are more broadly slowing economies as a result of the conflict that

is choking vital inputs, and increasingly higher prices.

Which brings us to PPI. Germany here again will be

illustrative with April PPI scheduled for release on Tuesday. Last month

factory gate prices rose 2.5 percent month on month. Other reports show

mounting concerns over increased production costs. The PMI reports for April

showed similar anecdotal concerns among producers.

US Preview

Housing Market in Focus

By Theresa Sheehan, Econoday Economist

Data related to the housing market will be the highlight of

the economic release calendar. It is typical for homebuying to pick up in the

spring months. It is the time of year when current homeowners start to list

their properties for sale, homebuilders are able to pick up the pace in milder

weather, and families make plans to move after the school year. However, the

supply of homes remains limited, especially in the more affordable price

ranges. Buyer traffic is limited to those households well qualified to get a

mortgage. Activity in the spring 2026 has been restrained despite a couple of

months of relatively low mortgage rates.

The Freddie Mac monthly average rate for a 30-year fixed

rate mortgage was a tempting 6.11 percent in January and February and close to

that at 6.18 percent in March. The increase to an average of 6.33 percent in

April and 6.37 percent in the first weeks of May still seems relatively

affordable compared to rates in the last three years. But rapidly rising home

prices mean even a few basis points can make the difference.

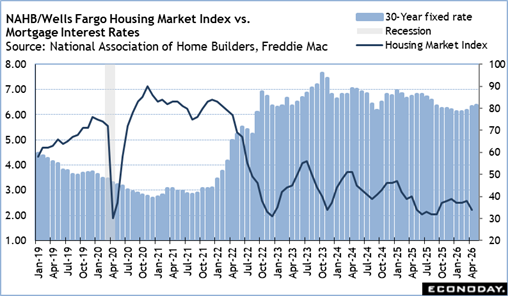

The NAHB/Wells Fargo housing market index (HMI) for May is

at 10:00 ET on Monday. The HMI reading for April was 34, a 4 point drop from

the prior month. The index has not been above the 50-mark that would signal

expansion since April 2024. Homebuilders have been having difficulty in finding

building lots, contending with labor shortages and rising wages, and

competition from increased supplies of existing homes on the market. At

present, low consumer confidence and challenges in properly pricing new homes against

a backdrop of inflation and delays along the supply chain are restraining

builder optimism. The May data for the HMI could be even softer if the increase

in mortgage rates is seen as reducing demand for new single-family homes.

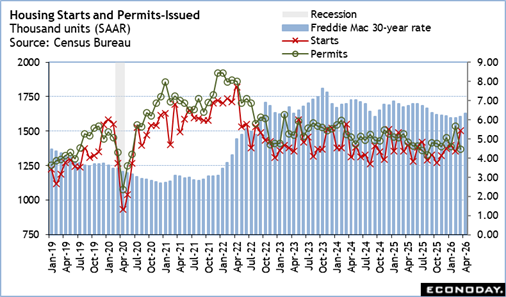

Data on housing starts and permits issued in April at 8:30

ET on Tuesday should reveal how builders' pessimism plays out in the actual

construction activity. Starts rebounded in March with a 10.8 percent increase

to a 1.502 million unit seasonally adjusted annual rate after bitterly cold

weather in kept starts down in the prior months. However, building permits fell

10.8 percent to 1.372 million units in March, suggesting less new construction

in the coming months.

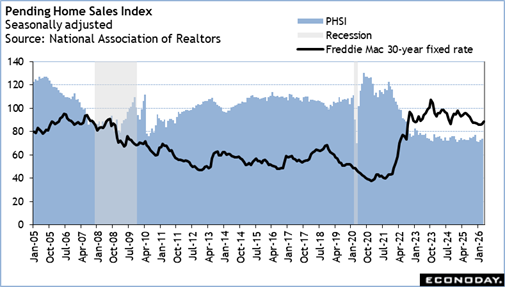

The NAR's pending home sales index (PHSI) at 10:00 ET on

Tuesday will point to the number of contracts signed but not yet closed in

April. Given that contracts will be using mortgages secured mostly in March and

early April, there is room for an increase for a third month in a row.

The Week Ahead: Econoday Consensus Forecasts

Monday

China Fixed Asset Investment for April (Mon 1000

CST; Mon 0200 GMT; Sun 2200 EDT)

Consensus Forecast, Year to Date on Y/Y Basis: 1.7%

Consensus Range, Year to Date on Y/Y Basis: 1.5% to 1.8%

FAI growth seen stuck at an anemic 1.7 percent in April from

1.7 percent in March.

China Industrial Production for April (Mon 1000

CST; Mon 0200 GMT; Sun 2200 EDT)

Consensus Forecast, Y/Y: 6.0%

Consensus Range, Y/Y: 5.5% to 6.0%

The consensus looks for output up a bit to 6.0 percent

increase on year from 5.7 percent in March.

China Retail Sales for April (Mon 1000 CST; Mon

0200 GMT; Sun 2200 EDT)

Consensus Forecast, Y/Y: 2.0%

Consensus Range, Y/Y: 1.8% to 2.2%

A slight improvement is expected to 2.0 percent growth on

year for April from 1.7 percent in March, still extremely weak for China.

US Housing Market Index for May (Mon 1000 EDT; Mon 1400

GMT)

Consensus Forecast, Index: 34

Consensus Range, Index: 34 to 35

The housing market remains stuck in doldrums. The Econoday

consensus looks for no change in the builder sentiment index at 34 in May from

34 in April.

Tuesday

Japan GDP for First Quarter (Tue 0850

JST; Mon 2350 GMT; Mon 1950 EDT)

Consensus Forecast, Q/Q: 0.5%

Consensus Range, Q/Q: 0.1% to 0.8%

Consensus Forecast, Annualized: 1.7%

Consensus Range, Annualized: 0.4% to 3.3%

Preliminary first-quarter GDP data is forecast to show the

economy expanded 0.5 percent from the previous quarter, or an annualized 1.7

percent, after rising 0.3 percent, or an annualized 1.3 percent, in

October-December, marking a second straight quarter of growth.

UK Labour Market Report for May (Tue 0700 BST; Tue 0600

GMT; Tue 0200 EDT)

Consensus Forecast, ILO Unemployment Rate: 4.9%

Consensus Range, ILO Unemployment Rate: 4.8% to 5.15

Consensus Forecast, Average Earnings - Y/Y: 3.7%

Consensus Range, Average Earnings - Y/Y: 3.6% to 3.8%

The jobless rate is expected unchanged at 4.9 percent and

earnings growth at 3.7 percent versus 3.8 percent in April.

Canada CPI for April (Tue 0830 EDT; Tue 1230 GMT)

Consensus Forecast, CPI - M/M: 0.7%

Consensus Range, CPI - M/M: 0.5% to 1.0%

Consensus Forecast, CPI - Y/Y: 3.1%

Consensus Range, CPI - Y/Y: 2.9% to 3.3%

Even with a cut in the gas tax in April, gas prices are

lifting CPI on month with expectations for a gain of 0.7 percent. On year,

removal of the carbon tax a year ago makes for a very unfriendly comparison.

That plus gas prices yields a consensus forecast of 3.1 percent.

US Housing Starts and Permits for April (Tue 0830 EDT;

Tue 1230 GMT)

Consensus Forecast, Starts - Annual Rate: 1.410 M

Consensus Range, Starts - Annual Rate: 1.350 M to 1.502

M

Consensus Forecast, Permits - Annual Rate: 1.380 M

Consensus Range, Permits - Annual Rate: 1.350 M to 1.450

M

Affordability weighs on housing with the consensus looking

for starts down to a 1.410 million unit rate from 1.502 million in March.

US Pending Home Sales Index for April (Tue 1000 EDT; Tue

1400 GMT)

Consensus Forecast, M/M: 0.9%

Consensus Range, M/M: 0.5% to 1.6%

Sales expected up 0.9 percent on the month.

Wednesday

China Loan Prime Rate for May (Wed 0915 CST; Wed 0115

GMT; Tue 2115 EDT)

Consensus Forecast, 1-Year Rate - Change: 0 bp

Consensus Range, 1-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 1-Year Rate - Level: 3.0%

Consensus Range, 1-Year Rate - Level: 3.0% to 3.0%

Consensus Forecast, 5-Year Rate - Change: 0 bp

Consensus Range, 5-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 5-Year Rate - Level: 3.50%

Consensus Range, 5-Year Rate - Level: 3.50% to 3.50%

Forecasters see the PBOC on hold again with stimulus efforts

focused elsewhere.

UK CPI for April (Wed 0700 BST; Wed 0600 GMT; Wed 0200

EDT)

Consensus Forecast, M/M: 0.8%

Consensus Range, M/M: 0.5% to 1.0%

Consensus Forecast, Y/Y: 2.9%

Consensus Range, Y/Y: 2.6% to 3.0%

Rising fuel costs expected to lift CPI by 0.8 percent on the

month and 2.9 percent on year.

Germany PPI for April (Wed 0800 CEST; Wed 0600 GMT;

Wed 0200 EDT)

Consensus Forecast, M/M: 1.1%

Consensus Range, M/M: 1.0% to 3.0%

Another big jump is the call with the consensus looking for

a gain of 1.1 percent in March after a 2.5 percent increase in March.

Eurozone HICP for April (Wed 1100 CEST; Wed 0900 GMT;

Wed 0500 EDT)

Consensus Forecast, HICP - Y/Y: 3.0%

Consensus Range, HICP - Y/Y: 3.0% to 3.0%

Consensus Forecast, Narrow Core - Y/Y: 2.2%

Consensus Range, Narrow Core - Y/Y: 2.2% to 2.2%

The consensus looks for no revision from the flash at 3.0

percent for April.

Thursday

Japan Merchandise Trade for April (Thu 0850 JST; Thu

2350 GMT; Wed 1950 EDT)

Consensus Forecast, Balance: -96.25 B

Consensus Range, Balance: -200.0 B to 67.80 B

Consensus Forecast, Imports - Y/Y: 8.8%

Consensus Range, Imports - Y/Y: 7.1% to 9.4%

Consensus Forecast, Exports - Y/Y: 9.4%

Consensus Range, Exports - Y/Y: 8.5% to 11.5%

Japan Machinery Orders for March (Thu 0850 JST; Thu

2350 GMT; Wed 1950 EDT)

Consensus Forecast, M/M: -13.2%

Consensus Range, M/M: -20.0% to -3.1%

Consensus Forecast, Y/Y: 4.4%

Consensus Range, Y/Y: -9.8% to 8.2%

Australia Labour Force Survey for April (Thu 1130

AET; Thu 0130 GMT; Wed 2130 EDT)

Consensus Forecast, Employment - M/M: 10K

Consensus Range, Employment - M/M: 10K to 28K

Consensus Forecast, Unemployment Rate: 4.3%

Consensus Range, Unemployment Rate: 4.2% to 4.4%

Forecasters see another modest rise, 10K in employment, with

the jobless rate steady at 4.3 percent.

France PMI Composite Flash for May (Thu 0815 CEST; Thu

0615 GMT; Thu 0215 EDT)

Consensus Forecast, Manufacturing Index: 52.5

Consensus Range, Manufacturing Index: 51.9 to 52.7

Consensus Forecast, Services Index: 46.0

Consensus Range, Services Index: 46.0 to 47.1

Some weakening seen with manufacturing expected at 52.5 in

the May flash from 52.8 in the April final. Services expected at 46.0 versus

46.5.

Germany PMI Composite Flash for May (Thu 0930 CEST; Thu

0730 GMT; Thu 0330 EDT)

Consensus Forecast, Manufacturing Index: 50.9

Consensus Range, Manufacturing Index: 50.5 to 51.6

Consensus Forecast, Services Index: 46.9

Consensus Range, Services Index: 45.5 to 47.9

Manufacturing expected slightly weaker at 50.9 versus 51.4

in April. Services seen flat in contractionary territory at 46.9.

Eurozone PMI Composite Flash for May (Thu 1000 CEST; Thu

0800 GMT; Thu 0400 EDT)

Consensus Forecast, Composite Index: 47.8

Consensus Range, Composite Index: 47.5 to 48.7

Consensus Forecast, Manufacturing Index: 51.7

Consensus Range, Manufacturing Index: 51.5 to 52.5

Consensus Forecast, Services Index: 47.6

Consensus Range, Services Index: 47.0 to 48.0

Another sluggish month seen with the composite at 47.8

versus 48.8 in April. Manufacturing expected at 51.7 versus 52.2 and services

flat at 47.6

UK PMI Composite Flash for May (Thu 0930 BST; Thu 0830

GMT; Thu 0430 EDT)

Consensus Forecast, Composite Index: 51.6

Consensus Range, Composite Index: 51.3 to 51.9

Consensus Forecast, Manufacturing Index: 52.8

Consensus Range, Manufacturing Index: 51.2 to 53.0

Consensus Forecast, Services Index: 51.7

Consensus Range, Services Index: 51.5 to 52.0

Some erosion seen with the composite down to 51.6 in May

from 52.6 in April, manufacturing down to 52.8 from 53.7 and services down to

51.7 from 52.7.

US Jobless Claims for Week 05/16 (Thu 0830 EDT; Thu

1230 GMT)

Consensus Forecast, Initial Claims - Level: 213 K

Consensus Range, Initial Claims - Level: 205 K to 215

K

Claims expected to continue edging up to 213K from 211K last

week and 199K the week before that.

US Philadelphia Fed Manufacturing Index for May (Thu

0830 EDT; Thu 1230 GMT)

Consensus Forecast, Index: 15.0

Consensus Range, Index: 12.0 to 20.0

A retreat to a moderate 15.0 figure is the call, down from

26.7 in April and 18.1 in March.

US PMI Composite Flash for May (Tue 0945 EDT; Tue

1345 GMT)

Consensus Forecast, Manufacturing Index: 53.5

Consensus Range, Manufacturing Index: 53.0 to 53.8

Consensus Forecast, Services Index: 51.2

Consensus Range, Services Index: 50.5 to 51.7

Manufacturing expected at 53.5 versus 54.5 and services at 51.2

versus 51.0.

Eurozone EC Consumer Confidence Flash for May (Thu

1600 CEST; Thu 1400 GMT; Thu 1000 EDT)

Consensus Forecast, Index: -21.0

Consensus Range, Index: -23.0 to -20.6

Confidence expected nearly unchanged at a gloomy minus 21.0

in the May flash.

Friday

Japan CPI for April (Fri 0830 JST; Thu 2330 GMT; Thu

1930 EDT)

Consensus Forecast, CPI - Y/Y: 1.8%

Consensus Range, CPI - Y/Y: 1.6% to 1.9%

Consensus Forecast, Ex-Fresh Food - Y/Y: 1.7%

Consensus Range, Ex-Fresh Food - Y/Y: 1.5% to 1.8%

Consensus Forecast, Ex-Fresh Food & Energy - Y/Y:

2.2%

Consensus Range, Ex-Fresh Food & Energy - Y/Y: 1.9%

to 2.3%

Germany GDP Flash for First Quarter (Fri 0800 CEST; Fri

0600 GMT; Fri 0200 EDT)

Consensus Forecast, Q/Q: 0.3%

Consensus Range, Q/Q: 0.2% to 0.3%

Consensus Forecast, Y/Y: 0.3%

Consensus Range, Y/Y: 0.3% to 0.5%

Growth expected modest but positive at 0.3 percent on

quarter and on year in Q1.

France Business Climate Indicator for May (Fri 0845

CEST; Fri 0645 GMT; Fri 0245 EDT)

Consensus Forecast, Index: 94.0

Consensus Range, Index: 92.0 to 96.7

Business sentiment seen unchanged at 94.0 in May from April.

Germany Ifo Survey for May (Tue 1000 CEST; Tue 0800

GMT; Tue 0400 EDT)

Consensus Forecast, Business Climate: 84.1

Consensus Range, Business Climate: 82.0 to 84.5

Consensus Forecast, Current Conditions: 85.0

Consensus Range, Current Conditions: 84.0 to 85.1

Consensus Forecast, Business Expectations: 83.2

Consensus Range, Business Expectations: 80.0 to 84.0

No recovery expected with the business climate index

expected weaker at 84.1 in May versus an already bleak 84.4 in April as the

energy shock weighs on business sentiment.

Canada Retail Sales for March (Fri 0830 EDT; Fri 1230

GMT)

Consensus Forecast, M/M: 0.6%

Consensus Range, M/M: 0.5% to 0.8%

As usual, forecasters agree with the Stats Canada advance

estimate that looks for sales up 0.6 percent in March.

US Consumer Sentiment for May (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, Index: 48.2

Consensus Range, Index: 47.9 to 49.0

Consensus Forecast, 1-Year Inflation Expectation: 4.5%

Consensus Range, 1-Year Inflation Expectation: 4.5% to

4.7%

Sentiment expected unrevised at a super-low 48.2 in the

final report for May, down from 49.8 in April and 52.2 a year ago. One-year

inflation expectations also expected unrevised at 4.5 percent.

US Leading Indicators for April (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, M/M: -0.3%

Consensus Range, M/M: -0.3% to -0.3%

Poor consumer sentiment and low building permits expected to

depress the index again after a similar result in February and March.

|