|

The Week Ahead: Highlights

US Preview

Labor Market Back in Focus

By Theresa Sheehan, Econoday Economist

The March 2 week includes several reports about the labor

market that will factor into the next decision about monetary policy at the

March 17-18 FOMC meeting and will color the update to the quarter forecasts in

the summary of economic projections (SEP). The February employment report at

8:30 ET on Friday, March 6 is the last and most important indicator about the

labor market that will be released before the start of the blackout period

around FOMC meeting (starts midnight on Saturday, March 7 and ends at midnight

on Thursday, March 19).

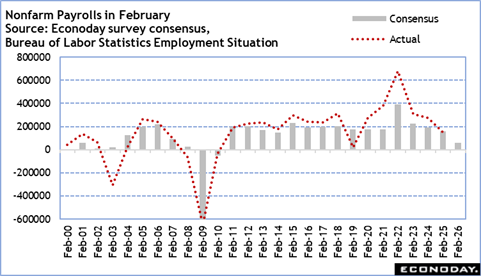

February payrolls are hard to estimate, in part because of

winter weather conditions. The weather may be a factor in the next report due

to a period of bitter cold for much of the country in late January and early

February. The cold was unusually present in much of the southeastern parts of

the country where normally some hints of spring would allow a pickup in outdoor

work. There was also major strike activity by the New York State Nurses

Association with about 42,000 members on strike for 41 days (January

12-February 21. This crosses the survey reference period and will affect the

headcounts in the health care sector. The nurses will be subtracted from the

February numbers but added back in in the March report. It might look

particularly bad with job gains in the health care sector being one of the few

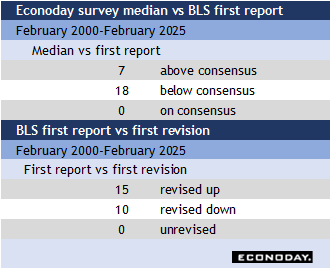

industries consistently adding to payrolls. The February employment report has

a strong tendency to come in below the market consensus, although it is

frequently revised higher in March. Winter weather and a mid-month holiday can

mean some initial underreporting.

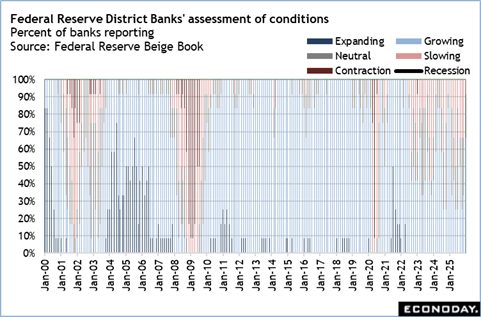

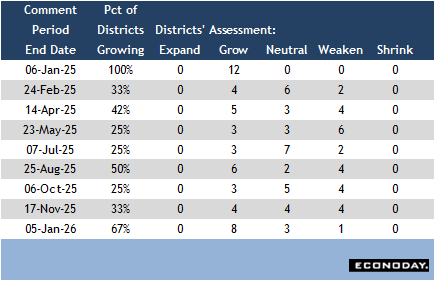

Also important for the outlook for the upcoming FOMC meeting

is the Fed's Beige Book is at 14:00 ET on Wednesday. The compilation of

anecdotal evidence about economic conditions across the 12 districts will cover

roughly the period from early January through mid-February. The Beige Book

released on January 14 was consistent with modest growth and an economy that

was shaking off the restraining effect of the chaotic rollout of higher tariffs

early in 2025 amid signs that tariff-driven inflation was abating. However, the

arrival of 2026 has brought other geopolitical uncertainties into play along

with concerns about the rapid adoption of AI technologies.

At this writing, neither the Senate Banking Committee nor

the House Financial Services Committee have announced a date for Fed Chair

Jerome Powell's semiannual monetary policy testimony. This becomes more urgent

as the preparatory work done by the Board of Governors - typically in late

January for testimony in the second week of February -- for their monetary

policy report gets outdated.

Also, the Senate Banking Committee has yet to schedule a

confirmation hearing for Kevin Warsh to become the next Chair of the Fed.

Oddly, the announcements of his nomination make no mention of a nomination as a

governor of the Fed board, which is a prerequisite for becoming chair. The

assumption is that Warsh will be nominated to the seat to which Stephen Miran

was appointed and not reconfirmed. Miran's term ended officially on January 31,

2026, but he can remain on the board until another governor is nominated and

confirmed. The current unexpired term runs for 14 years through January 31,

2040. Sen. Thomas Tillis of North Carolina, a key member of the Senate Banking

Committee, has said he will prevent any Fed nomination from proceeding until

the president's threat to prosecute Powell ends.

Europe Preview

SNB Decision Highlights European Week

By Marco Babic, Econoday Economist

Europe's week starts off Monday with the decision from the

Swiss National Bank on its policy rate now at zero percent. The SNB moved rates

into negative territory before, but so far has seemed reluctant to do so again.

The Swiss central bank will certainly consider economic

conditions, which currently show a relatively stagnant economy with no

inflation. At the same time, negative interest rates were a burden on both

banks and clients when they have to actually pay for the privilege of holding

cash. When negative rates were policy, a number of wealth managers and banks

said that higher interest rates were actually in their best interests.

So, what is a central bank to do? The United States has once

again thrown a spanner into the works after the Supreme Court determined that

the tariffs imposed by the Trump administration are illegal. The question is

whether the Swiss government and, for that matter, the European Union

re-engages the US on tariffs. For, now the EU has put its trade agreement on

hold pending more clarity. There is no reason to think the Swiss government

won't do likewise.

Bearing all that in mind, the SNB will likely hold rates at

zero, stand pat, and let events play out. Inflation is not an issue, save for

volatility around energy prices. At the same time, the strength of the Swiss

franc is keeping imported inflation at bay.

Preliminary inflation data is set for release for the

Eurozone and also the major economies, and there is nothing to suggest that the

results will trouble the ECB. It will be interesting to see of the guardians of

the euro in Frankfurt will have discussed the tariff situation when they

release the minutes on Thursday of their previous meeting.

The rest of the has final PMI readings for the main

economies, which are not expected to stray to far, if at all, from preliminary

numbers, while Italy final GDP on Wednesday will give more details about the

breakdown of economic performance, with trade of particular interest.

Asia-Pacific Preview

Purchasing Managers Reports in Focus; China Data Returns

By Brian Jackson, Econoday Economist

PMI surveys will be the main focus of the Asia-Pacific data

calendar, particularly the Chinese surveys. Many key Chinese indicators are not

published separately for January and February because of distortions caused by

the timing of lunar new year holidays, meaning there has been little

information published in recent weeks about conditions there. Surveys for other

Asian nations will also likely be impacted to some extent by lunar new year

holidays.

Australia will publish monthly trade and household spending

data and the quarterly GDP release, while South Korea will report monthly

trade, industrial production, retail sales and inflation data. Taiwan inflation

and industrial production data will be published late in the week ahead of the

quarterly policy meeting in mid-March.

The Week Ahead: Econoday Consensus Forecasts

Monday

India PMI Manufacturing Final for February (Mon 1030

IST; Mon 0500 GMT; Mon 0000 EST)

Consensus Forecast, Level: 57.5

Consensus Range, Level: 57.5 to 57.5

The consensus sees no revision for the final from 57.5 in

the flash, up from 55.4 in January final.

Germany Retail Sales for January (Mon 0800 CET; Mon 0700

GMT; Mon 0200 EST)

Consensus Forecast, M/M: -0.2%

Consensus Range, M/M: -0.5% to 0.5%

Sales are sluggish, expected to retreat 0.2 percent in

January after rising by 0.1 percent in December on month.

Eurozone PMI Manufacturing Final for February (Mon 0900

CET; Mon 0800 GMT; Mon 0300 EST)

Consensus Forecast, Index: 50.8

Consensus Range, Index: 50.8 to 50.8

The consensus sees no revision in the final for February

from the flash at 50.8 and up from 49.5 in January final.

Switzerland SNB Monetary Policy Assessment for March (Mon

0930 CET; Mon 0830 GMT; Mon 0330 EST)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 0.0%

Consensus Range, Level: 0.0% to 0.0%

The consensus sees no rate change.

France PMI Manufacturing Final for February (Mon 0950

CET; Mon 0850 GMT; Mon 0350 EST)

Consensus Forecast, Index: 49.9

Consensus Range, Index: 49.9 to 498.9

The consensus sees no revision in the final for February

from the flash at 49.9 and versus 51.2 in January final.

Germany PMI Manufacturing Final for February (Mon 0955

CET; Mon 0755 GMT; Mon 0355 EST)

Consensus Forecast, Index: 50.7

Consensus Range, Index: 50.7 to 50.7

The consensus sees no revision in the final for February

from the flash at 50.7 and up from 49.1 in January final.

UK PMI Manufacturing Final for February (Mon 0930

BST; Mon 0930 GMT; Mon 0430 EST)

Consensus Forecast, Index: 52.0

Consensus Range, Index: 52.0 to 52.0

The consensus sees no revision in the final for February

from the flash at 52.0 and versus 51.8 in January final.

US PMI Manufacturing Final for February (Mon 0945

EST; Mon 1445 GMT)

Consensus Forecast, Index: 51.2

Consensus Range, Index: 51.2 to 51.2

The consensus sees no revision in the final for February

from the flash at 51.2 and down from 52.4 in January final.

US ISM Manufacturing Index for February (Mon 1000

EST; Mon 1500 GMT)

Consensus Forecast, Index: 51.8

Consensus Range, Index: 50.5 to 53.0

Manufacturing seen barely expansionary at 51.8 in February

versus 52.6 in January.

Tuesday

Japan Unemployment Rate for January (Tue 0830 JST; Mon

2330 GMT; Mon 1830 EST)

Consensus Forecast, Rate: 2.6%

Consensus Range, Rate: 2.5% to 2.6%

Japan's seasonally adjusted unemployment rate is expected to

remain unchanged for a sixth consecutive month at 2.6 percent in January, as

persistent labor shortages across a wide range of industries continue to

support payrolls.

In December, employment rose for a 41st straight

year-on-year increase, with the number of employed persons up 130,000 from a

year earlier to 68.42 million. Many companies continue to seek qualified

workers, particularly in hospitals, construction firms, hotels and restaurants.

By contrast, manufacturers and the wholesale and retail sectors continued to

reduce their workforces.

Meanwhile, the number of unemployed people increased for a

fifth consecutive month in December. By reason for seeking employment compared

with the same month a year earlier, the number of those who left jobs for

employer- or business-related reasons rose by 10,000, while voluntary job

leavers fell by 10,000. The number of new job seekers increased by 110,000.

US Motor Vehicle Sales for February (ANYTIME)

Consensus Forecast, Total Vehicle Sale - Annual Rate:

15.3 M

Consensus Range, Total Vehicle Sale - Annual Rate: 15.1

M to 15.8 M

The consensus sees sales up to an annual 15.3 million unit

rate from 14.9 million in January.

Eurozone HICP Flash for February (TUE 1100 CET; TUE

1000 GMT; TUE 0500 EST)

Consensus Forecast, HICP - Y/Y: 1.7%

Consensus Range, HICP - Y/Y: 1.7% to 1.8%

Consensus Forecast, Narrow Core - Y/Y: 2.2%

Consensus Range, Narrow Core - Y/Y: 2.0% to 2.2%

The consensus sees HICP up 1.7percent on year and the narrow

core up 2.2 percent, unchanged from the January final.

Italy CPI for February (Tue 1100 CET; Tue 1000 GMT; Tue

0500 EST)

Consensus Forecast, Y/Y: 1.1%

Consensus Range, Y/Y: 1.1% to 1.1%

CPI expected up 1.1 percent on year in the February

preliminary report versus 1.0 percent in the January final.

Wednesday

Australia GDP for Fourth Quarter (Wed 1130 AET; Wed 0030

GMT; Tue 1930 EST)

Consensus Forecast, Q/Q: 0.8%

Consensus Range, Q/Q: 0.5% to 0.9%

Growth seen better at 0.8 percent in Q4 from Q3 versus 0.4

percent in Q3 as consumer spending and housing investment pick up steam.

China CFLP Composite PMI for February (Wed 0930 CST; Wed

0130 GMT; Tue 2030 EST)

Consensus Forecast, Manufacturing Index: 49.1

Consensus Range, Manufacturing Index: 49.0 to 49.9

Consensus Forecast, Non-Manufacturing Index: 49.7

Consensus Range, Non-Manufacturing Index: 49.5 to 50.0

Slow contraction continuing with manufacturing expected marginally

weaker at 49.1 in February versus 49.3 in January and services better at 49.7 from

49.4 in January.

China PMI Composite for February (Wed 0945 CST; Wed

0145 GMT; Tue 2045 EST)

Consensus Forecast, Services Index: 52.3

Consensus Range, Services Index: 51.7 to 52.4

The consensus looks for services flat at 52.3 in February

from January, suggesting modest expansion in services business, slightly better

than the official CFLP report showing no growth.

Eurozone PMI Composite Final for March (Wed 0900 CET;

Wed 0800 GMT; Wed 0300 EST)

Consensus Forecast, Composite Index: 51.9

Consensus Range, Composite Index: 51.9 to 51.9

Consensus Forecast, Services Index: 51.8

Consensus Range, Services Index: 51.8 to 51.8

The consensus sees no revision in the final from the flash

at 51.9 for composite and 51.8 for services in the February final.

Germany PMI Composite Final for February (Wed 0955

CET; Wed 0855 GMT; Wed 0355 EST)

Consensus Forecast, Composite Index: 53.1

Consensus Range, Composite Index: 53.1 to 53.1

Consensus Forecast, Services Index: 53.4

Consensus Range, Services Index: 53.4 to 53.4

The consensus sees no revision in the final from the flash

at 53.1 for composite and 53.4 for services in the February final.

UK PMI Composite Final for February (Wed 0930 BST;

Wed 0930 GMT; Wed 0430 EST)

Consensus Forecast, Composite Index: 53.9

Consensus Range, Composite Index: 53.9 to 53.9

Consensus Forecast, Services Index: 53.9

Consensus Range, Services Index: 53.9 to 53.9

The consensus sees no revision in the final from the flash

at 53.9 for composite and 53.9 for services in the February final.

Eurozone Unemployment Rate for February (Wed 1100

CEST; Wed 1000 GMT; Wed 0500 EDT)

Consensus Forecast, Rate: 6.2%

Consensus Range, Rate: 6.2% to 6.3%

No change expected in the jobless rate.

US ADP Employment Report for February (Wed 0815 EST;

Wed 1315 GMT)

Consensus Forecast, Private Payrolls - M/M: 43K

Consensus Range, Private Payrolls - M/M: 19K to 55K

Private payrolls expected up a meager 43K in February after

22K in January.

US PMI Services Final for February (Wed 0945 EST; Wed

1445 GMT)

Consensus Forecast, Index: 52.3

Consensus Range, Index: 52.0 to 52.3

No revision expected in the final February report from the

flash for PMI services at 52.3.

US ISM Services Index for February (Wed 1000 GMT; Wed

1500 EST)

Consensus Forecast, Services Index: 53.6

Consensus Range, Services Index: 52.0 to 54.2

Forecasters see growth stable with an index at 53.6 versus

53.8 in January.

Thursday

Australia International Trade in Goods for January (Thu

1130 AET; Thu 0030 GMT; Wed 1930 EST)

Consensus Forecast, Balance: A$4.1 B

Consensus Range, Balance: A$3.1 B to A$5.0 B

The consensus looks for a slight widening in the surplus to

A$4.1 billion from $3.373 billion a month earlier.

Australia Household Spending for January (Thu 1130

AET; Thu 0030 GMT; Wed 1930 EST)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: 0.0% to 0.8%

The consensus sees a return to moderate growth for spending

at a 0.4 percent increase on the month after a decline of 0.4 percent in the

previous month.

France Industrial Production for January (Thu 0845

CET; Thu 0745 GMT; Thu 0245 EST)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: 0.4% to 1.0%

Sales seen rebounding by 0.5 percent in January after

dropping 0.8 percent in December.

Eurozone Retail Sales for January (Thu 1100 CEST; Thu

1000 GMT; Thu 0500 EST)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: -0.1% to 0.6%

Consensus Forecast, Y/Y: 1.7%

Consensus Range, Y/Y: 1.4% to 2.1%

Sales expected up 0.2 percent on the month and 1.7 percent

on year.

US Jobless Claims for Week 02/28 (Thu 0830 GMT; Wed

1330 EST)

Consensus Forecast, Initial Claims - Level: 215K

Consensus Range, Initial Claims - Level: 210K to 220K

Claims seen at 215K, up from 212K last week.

US Productivity and Costs for Fourth Quarter Prelim. (Thu

0830 EST; Thu 1330 GMT)

Consensus Forecast, Nonfarm Productivity - Annual Rate:

1.9%

Consensus Range, Nonfarm Productivity - Annual Rate: 1.5%

to 4.0%

Consensus Forecast, Unit Labor Costs - Annual Rate: 2.1%

Consensus Range, Unit Labor Costs - Annual Rate: -0.7%

to 2.6%

The delayed first reading for Q4 expected to show much

slower productivity growth at 1.9 percent versus 4.9 percent in Q3 and ULC up

2.1 percent versus a decrease of 1.9 percent in Q3.

US Imports and Export Prices for January (Thu 0830

EST; Thu 1330 GMT)

Consensus Forecast, Import Prices - M/M: 0.1%

Consensus Range, Import Prices - M/M: -0.1% to 0.2%

Consensus Forecast, Export Prices - M/M: 0.2%

Consensus Range, Export Prices - M/M: 0.0% to 0.4%

Import prices seen up 0.1 percent and export prices up 0.2

percent in January on the month.

Friday

South Korea CPI for February (Fri 0800 KST; Thu 2300

GMT; Thu 1800 EST)

Consensus Forecast, CPI - M/M: 0.4%

Consensus Range, CPI - M/M: 0.2% to 0.5%

Consensus Forecast, CPI - Y/Y: 2.1%

Consensus Range, CPI - Y/Y: 1.9% to 2.2%

CPI expected up 0.4 percent on the month and 2.1 percent on

year in February.

Germany Manufacturing Orders for January (Fri 0800

CET; Fri 0700 GMT; Fri 0200 EST)

Consensus Forecast, M/M: -5.0%

Consensus Range, M/M: -10.0% to -3.0%

Consensus Forecast, Y/Y: 13.1%

Consensus Range, Y/Y: 12.0% to 13.2%

Sales volatility continues with sales seen down 5.0 percent

on the month after a 7.8 percent jump in the previous month.

Eurozone GDP Flash for Fourth Quarter (Fri 1100 CET; Fri

1000 GMT; Fri 0500 EST)

Consensus Forecast, Q/Q: 0.3%

Consensus Range, Q/Q: 0.3% to 0.3%

Consensus Forecast, Y/Y: 1.3%

Consensus Range, Y/Y: 1.3% to 1.3%

No revision from the last report expected with GDP up 0.3

percent on quarter and 1.3 percent on year.

US Employment Situation for February (Fri 0830 EST;

Fri 1330 GMT)

Consensus Forecast, Nonfarm Payrolls - M/M: 60K

Consensus Range, Nonfarm Payrolls - M/M: 35K to 125K

Consensus Forecast, Unemployment Rate: 4.4%

Consensus Range, Unemployment Rate: 4.3% to 4.4%

Consensus Forecast, Private Payrolls - M/M: 65K

Consensus Range, Private Payrolls - M/M: 49K to 80K

Consensus Forecast, Average Hourly Earnings - M/M: 0.3%

Consensus Range, Average Hourly Earnings - M/M: 0.3%

to 0.3%

Consensus Forecast, Average Hourly Earnings - Y/Y: 3.7%

Consensus Range, Average Hourly Earnings - Y/Y: 3.6%

to 3.8%

Consensus Forecast, Average Workweek Hours: 34.3

Consensus Range, Average Workweek: 34.2 to 34.3

Jobs expected up 60K, a moderate showing these days, with

the jobless rate up a tick at 4.4 percent versus 4.3 percent in January.

US Retail Sales for January (Fri 0830 EST; Fri 1330

GMT)

Consensus Forecast, Retail Sales - M/M: -0.4%

Consensus Range, Retail Sales - M/M: -0.8% to 0.4%

Consensus Forecast, Ex-Vehicles - M/M: 0.1%

Consensus Range, Ex-Vehicles - M/M: -0.4% to 0.6%

Sales expected basically flat, up 0.1 percent, ex-autos. Not

impressive, especially as these are nominal numbers.

US Business Inventories for December (Fri 1000 EST; Fri

1500 GMT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: -0.1% to 0.1%

Inventories seen flat in December after edging up 0.1

percent in November.

US Consumer Credit for January (Fri 1500 EST; Fri

2000 GMT)

Consensus Forecast, M/M: $ 11.1 B

Consensus Range, M/M: $8.0 B to $12.0 B

A trend like rise of $11.1 billion in the call after an unusually

large $24 billion increase in the previous month.

|