|

The Week Ahead: Highlights

Asia-Pacific Preview

Australia Inflation Report in Focus

By Brian Jackson, Econoday Economist

Australian inflation data for January will be the main focus

in the Asia-Pacific region. December data showed headline inflation above the

Reserve Bank of Australia's target range of two percent to three percent for

the fourth consecutive month, largely reflecting the impact of higher

electricity prices. The RBA hiked policy rates earlier this month, reflecting

their assessment that inflation will be above the target range "for some time".

Quarterly investment data will also be published next week.

The Bank of Korea meets, just over a month after officials

there left policy rates on hold in their previous meeting. Data released since

then have shown weakness in industrial production but steady core inflation,

suggesting that policy stability will continue at the upcoming meeting.

Singapore industrial production and inflation data are also

scheduled for release in the week ahead, with Hong Kong reporting trade,

inflation and GDP data. India will report industrial production and GDP data.

US Preview

On a Quiet Data Week, Watch for Fed Bank Business

Conditions Surveys

By Theresa Sheehan, Econoday Economist

The data release schedule continues to play catch-up in the

February 20 week. The delayed report for December new orders for factory goods

is at 10:00 ET on Monday. Wholesale trade for December is at 10:00 ET on

Tuesday. Friday sees the release of the combined November and December reports

for construction spending.

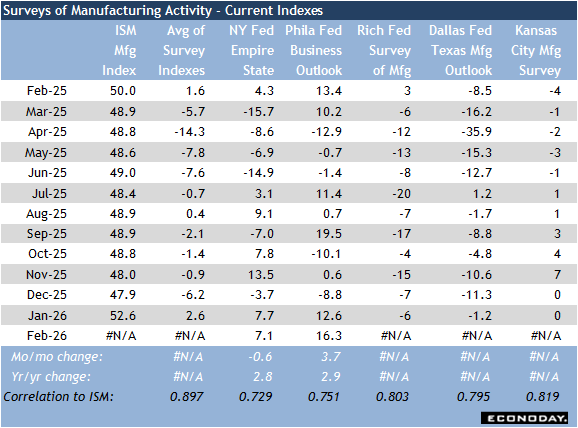

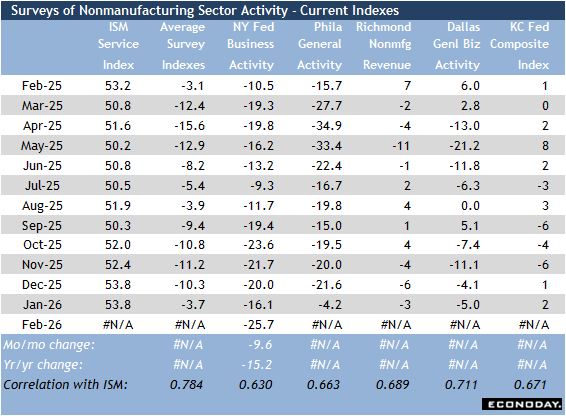

There is little in the way of first-tier data reports in the

week. What may prove most interesting are the monthly surveys of manufacturing

and services for February from five Fed district banks. This may provide some

insight into economic conditions at the mid-point of the first quarter 2026

after the advance estimate of GDP for the fourth quarter 2025 came in at a

disappointing up 1.4 percent.

The Dallas Fed survey of manufacturing is Monday at 10:30 ET

followed by the service sector survey at 10:30 ET on Tuesday. The Richmond Fed

releases its surveys of manufacturing and nonmanufacturing at 10:00 ET on

Tuesday. The Kansas City Fed survey of manufacturing is set for Thursday at

11:00 ET and the service sector survey is at 11:00 ET on Friday. The

manufacturing and nonmanufacturing surveys from the New York Fed were released

on February 17 and 18, respectively. The Philadelphia survey of manufacturing

was reported on February 19 and the services sector survey will be at 8:30 ET

on Tuesday.

The earlier data from New York and Philadelphia suggest that

conditions in the factory sector are relatively stable in February. With only

the New York report it is harder to assess current conditions for services. The

New York business activity index points to weakening with a 9.6 point decline

to minus 25.7. However, this drop may well be an artifact of the extreme cold

in the Northeast that has caused delays and shutdowns for many consumers and

businesses.

The Week Ahead: Econoday Consensus Forecasts

Monday

New Zealand Retail Trade for Fourth Quarter (Mon 1045

NZDT; Sun 2145 GMT; Sun 1645 EST)

Consensus Forecast, Q/Q: 0.6%

Consensus Range, Q/Q: 0.2% to 0.7%

The consensus looks for retail trade to rise 0.6 percent in

the fourth quarter from the third after rising 1.9 percent in Q3 from Q2.

Falling interest rates continue to support interest-sensitive spending.

Singapore CPI for January (Mon 1300 CST; Mon 0500

GMT; Mon 0000 EST)

Consensus Forecast, Y/Y: 1.6%

Consensus Range, Y/Y: 1.3% to 1.7%

The consensus sees CPI up 1.6 percent on year in January

after rising 1.2 percent in December.

Germany Ifo Survey for February (Mon 1000 CET; Mon

0900 GMT; Mon 0400 EST)

Consensus Forecast, Business Climate: 88.4

Consensus Range, Business Climate: 87.3 to 89.2

Consensus Forecast, Current Conditions: 86.1

Consensus Range, Current Conditions: 85.5 to 87.5

Consensus Forecast, Business Expectations: 90.0

Consensus Range, Business Expectations: 89.1 to 91.0

Sentiment seen edging up with business climate at 88.4

versus 87.6 in the prior month. Current conditions seen at 86.1 versus 85.7 and

expectations at 90.0 versus 89.5.

Italy CPI for January (Mon 1100 CET; Mon 1000 GMT;

Mon 0500 EST)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: % to

Consensus Forecast, Y/Y: 1.0%

Consensus Range, Y/Y: 1.0% to 1.0%

The consensus sees no revision for January final from gains

of 0.4 percent on month and 1.0 percent on year in the flash.

United States Factory Orders for December (Mon 1000

EST; Mon 1500 GMT)

Consensus Forecast, M/M: -0.7%

Consensus Range, M/M: -1.5% to 1.0

The consensus looks for orders down 0.7 percent in December

after a 2.7 percent rise in November. Durable goods orders were already

reported down 1.4 percent on falling aircraft orders.

Tuesday

China Loan Prime Rate for February (Tue 0915 CST; Tue

0115 GMT; Tue 2015 EST)

Consensus Forecast, 1-Year Rate - Change: 0 bp

Consensus Range, 1-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 1-Year Rate - Level: 3.00%

Consensus Range, 1-Year Rate - Level: 3.00% to 3.00%

Consensus Forecast, 5-Year Rate - Change: 0 bp

Consensus Range, 5-Year Rate - Change: 0 bp to 0 bp

Consensus Forecast, 5-Year Rate - Level: 3.50%

Consensus Range, 5-Year Rate - Level: 3.50% to 3.50%

The consensus sees no action from the PBOC as Chinese

authorities are using fiscal measures to boost demand.

US Case-Shiller Home Price Index for December (Tue

0900 EST; Tue 1400 GMT)

Consensus Forecast, 20-City Adjusted - M/M: 0.3%

Consensus Range, 20-City Adjusted - M/M: 0.2% to 0.3%

Consensus Forecast, 20-City Unadjusted - Y/Y: 1.4%

Consensus Range, 20-City Unadjusted - Y/Y: 1.0% to

1.6%

A trend-like 0.3 percent rise on month and the same 1.4

percent increase on year from last month is the call.

US FHFA House Price Index for December (Tue 0900 EST;

Tue 1400 GMT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: 0.2% to 1.0%

A moderate 0.3 percent increase on the month is expected.

US Consumer Confidence for February (Tue 1000 EST;

Tue 1500 GMT)

Consensus Forecast, Index: 88.0

Consensus Range, Index: 85.0 to 90.5

Forecasters think confidence recovered a bit after January's

surprising drop. Consumer confidence seen at 88.0 in February versus 84.5 in

January.

Wednesday

Australia Monthly CPI for January (Wed 1130 AET; Wed

0030 GMT; Tue 1930 EST)

Consensus Forecast, Y/Y: 3.7%

Consensus Range, Y/Y: 3.3% to 4.0%

CPI is expected lower at 3.7 percent on year in January

compared with 3.8 percent in December. Lower prices for auto fuel and clothing

are helping reduce price pressure despite increases for food, health costs, and

electricity.

Germany GfK Consumer Climate for March (Wed 1000 CET;

Wed 0900 GMT; Wed 0400 EST)

Consensus Forecast, Index: -23.1

Consensus Range, Index: -25.0 to -22.5

Sentiment index expected marginally better at minus 23.1 in

March versus minus 24.1 in February.

Germany GDP for Fourth Quarter (Wed 0800 CET; Wed

0700 GMT; Wed 0200 EST)

Consensus Forecast, Q/Q: 0.3%

Consensus Range, Q/Q: 0.3% to 0.5%

Consensus Forecast, Y/Y: 0.4%

Consensus Range, Y/Y: 0.4% to 0.4%

The consensus looks for Q4 GDP unrevised from the flash at

0.3 percent on month and 0.4 percent on year.

Eurozone HICP for January (Wed 1100 CET; Wed 1000

GMT; Wed 0500 EST)

Consensus Forecast, HICP - Y/Y: 1.7%

Consensus Range, HICP - Y/Y: 1.7% to 1.7%

Consensus Forecast, Narrow Core - Y/Y: 2.2%

Consensus Range, Narrow Core - Y/Y: 2.2% to 2.3%

The consensus looks for January HICP unrevised from the

flash at an increase of 1.7 percent on year with narrow core unrevised at 2.2

percent.

Thursday

Australia Capital Expenditures for April (Thu 1130

AET; Thu 0030 GMT; Wed 1930 EST)

Consensus Forecast, Q/Q: -0.3%

Consensus Range, Q/Q: -3.0% to 1.5%

The consensus sees capex down 0.3 percent on quarter in Q4

after huge 6.4 percent growth in Q3. A retreat in data center spending is

culprit.

South Korea Bank of Korea Announcement (Thu 1000 KST;

Thu 0100 GMT; Wed 2000 EST)

Consensus Forecast, Change: 0 bp

Consensus Range, Change: 0 bp to 0 bp

Consensus Forecast, Level: 2.50%

Consensus Range, Level: 2.50% to 2.50%

The consensus looks for no rate change until next year.

Singapore Industrial Production for January (Thu 1300

CST; Thu 0500 GMT; Thu 0000 EST)

Consensus Forecast, Y/Y: 12.1%

Consensus Range, Y/Y: 7.5% to 20.0%

Output expected up by 12.1 percent on year in January after

rising 8.3 percent in December.

Eurozone M3 Money Supply for January (Thu 1000 CET;

Thu 0900 GMT; Thu 0400 EST)

Consensus Forecast, Y/Y-3-Month Moving Average: 2.9%

Consensus Range, Y/Y-3-Month Moving Average: 2.8% to 2.9%

Money supply growth seen at the same 2.9 percent in January as

in December.

Eurozone EC Economic Sentiment for February (Thu 1100

CET; Thu 1000 GMT; Thu 0500 EST)

Consensus Forecast, Economic Sentiment: 99.6

Consensus Range, Economic Sentiment: 98.5 to 100.0

Consensus Forecast, Industry Sentiment: -6.6

Consensus Range, Industry Sentiment: -7.0 to -6.0

Not much change expected. Economic sentiment predicted at 99.6

for February versus 99.4 in January. Industry sentiment seen at minus 6.6

versus minus 6.8 in January.

US Jobless Claims for Week 2/21 (Thu 0830 EST; Thu

1330 GMT)

Consensus Forecast, Initial Claims - Level: 215K

Consensus Range, Initial Claims - Level: 212K to 221K

Claims back up at 215K in the latest week from an

unexpectedly low 206K in the previous week.

US Wholesale Inventories (Advance) for January (Thu

0830 EST; Thu 1330 GMT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.1% to 0.2%

The consensus sees inventories up 0.2 percent on the month.

Friday

Japan Tokyo CPI for February (Fri 0830 JST; Thu 2330

GMT; Thu 1830 EST)

Consensus Forecast, CPI - Y/Y: 1.4%

Consensus Range, CPI - Y/Y: 1.2% to 1.5%

Consensus Forecast, Ex-Fresh Food - Y/Y: 1.7%

Consensus Range, Ex-Fresh Food - Y/Y: 1.6% to 1.8%

Consensus Forecast, Ex-Fresh Food & Energy - Y/Y:

2.3%

Consensus Range, Ex-Fresh Food & Energy - Y/Y: 2.3%

to 2.4%

Consumer inflation in Tokyo, a leading indicator of

nationwide price trends, is expected to fall below the Bank of Japan's closely

watched 2 percent target in two of the key measures in February, driven mainly

by government subsidies aimed at easing the burden of electricity and city gas

charges.

In addition, slowing food and energy prices, along with

softer retail prices at supermarkets and other stores, are seen putting

downward pressure on Tokyo's consumer price index.

As a result, the core CPI, which excludes fresh food, is

forecast to rise 1.7 percent on the year in February, easing from 2.0 percent

in January and marking the first drop below the 2 percent level since October

2024. That would also be the slowest increase since March 2022, when it rose

0.9 percent.

Elsewhere, the headline CPI is seen slowing to 1.4 percent,

the lowest level in nearly four years, from 1.5 percent a month earlier. The

core-core index, which excludes fresh food and energy, is expected to rise 2.3

percent, edging down from a 2.4 percent increase in January. All three measures

have remained below 3 percent since June after retreating from earlier peaks.

Japan Industrial Production for January (Fri 0850

JST; Thu 2350 GMT; Thu 1850 EST)

Consensus Forecast, M/M: 5.3%

Consensus Range, M/M: 4.0% to 7.0%

Consensus Forecast, Y/Y: 5.2%

Consensus Range, Y/Y: 4.2% to 7.2%

Japan's industrial production is expected to rebound sharply

on the month in January, marking the first increase in three months, as

front-loaded activity ahead of the Lunar New Year prompted a surge in output.

January production is forecast to jump about 5.3 percent

after edging down 0.1 percent in December. In December, the impact of stiff

U.S. tariffs on automobiles and metals imposed in the fourth quarter of last

year undermined exports and weighed on output, although the pace of decline was

easing.

On a year-on-year basis, January output is also expected to

rise for a second straight month, up 5.2 percent after a 2.6 percent increase

in December.

Japan Retail Sales for January (Fri 0850 JST; Thu

2350 GMT; Thu 1850 EST)

Consensus Forecast, M/M: 2.1%

Consensus Range, M/M: 1.6% to 3.0%

Consensus Forecast, Y/Y: 0.1%

Consensus Range, Y/Y: -1.2% to 2.5%

Japan's retail sales are projected to inch up on the year in

January after unexpectedly declining in the previous month, dragged down by

lower fuel costs and weaker clothing sales amid sluggish department store

performance.

Retail sales are seen rising a slim 0.1 percent from a year

earlier in January, following a 0.9 percent drop the previous month.

Department store sales showed signs of recovery in January

as consumption picked up during the year-end and New Year holiday period.

Overall sales, however, remained under pressure as a slowdown in automobile

sales, combined with falling gasoline prices, weighed on fuel-related revenue.

On a month-on-month basis, retail sales are expected to

increase 2.1 percent on a seasonally adjusted basis, reversing a 2.0 percent

decline in December.

France GDP for Fourth Quarter (Fri 0845 CET; Fri 0745

GMT; Fri 0245)

Consensus Forecast, Q/Q: 0.2%

Consensus Range, Q/Q: 0.2% to 0.2%

Consensus Forecast, Y/Y: 1.1%

Consensus Range, Y/Y: 1.1% to 1.1%

GDP growth expected unrevised from 0.2 percent on quarter

and 1.1 percent on year in Q4.

Switzerland GDP for Fourth Quarter (Fri 0900 CET; Fri

0800 GMT; Fri 0300 EST)

Consensus Forecast, Q/Q-Adjusted: 0.2%

Consensus Range, Q/Q-Adjusted: 0.1% to 0.3%

GDP expected up 0.2 percent on quarter.

Germany Unemployment Rate for January (Fri 0955 CET;

Fri 0855 GMT; Fri 0355 EST)

Consensus Forecast, Rate: 6.3%

Consensus Range, Rate: 6.3% to 6.3%

Another month of no change at 6.3 percent for the jobless

rate,

India GDP for Fourth Quarter (Fri 1730 IST; Fri 1200

GMT; Fri 0700 EST)

Consensus Forecast, Y/Y: 7.3%

Consensus Range, Y/Y: 7.1% to 7.6%

Growth seen at 7.3 percent in Q4 after 8.2 percent in Q3 on

year.

Germany CPI for February (Fri 1400 CET; Fri 1300 GMT;

Fri 0800 EST)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: 0.3% to 0.5%

Consensus Forecast, Y/Y: 2.0%

Consensus Range, Y/Y: 2.0% to 2.1%

Consensus Forecast, HICP - M/M: 0.5%

Consensus Range, HICP - M/M: 0.4% to 0.5%

Consensus Forecast, HICP - Y/Y: 2.1%

Consensus Range, HICP - Y/Y: 2.0% to 2.1%

CPI seen at 0.4 percent on month and 2.0 percent on year in

February after increasing 0.1 percent on month and 2.1 percent on year in

January.

Canada Monthly GDP for December (Fri 0830 EST; Fri

1330 GMT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: 0.0% to 0.2%

More negligible growth seen in December, 0.1 percent on the

month.

Canada GDP for Fourth Quarter (Fri 0830 EST; Fri 1330

GMT)

Consensus Forecast, Annual Rate: -0.2%

Consensus Range, Annual Rate: -0.4% to 0.1%

The consensus says the economy stalled in Q4 and shrank at

an annualized 0.2 percent.

US PPI-Final Demand for January (Fri 0830 EST;

Fri 1330 GMT)

Consensus Forecast, PPI-FD - M/M: 0.3%

Consensus Range, PPI-FD - M/M: 0.2% to 0.5%

Consensus Forecast, PPI - Y/Y: 2.8%

Consensus Range, PPI - Y/Y: 2.6% to 2.9%

Consensus Forecast, Ex-Food & Energy - M/M: 0.3%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to 0.3%

January expected to show monthly increases of 0.3 percent

for total and 0.3 percent for core.

US Chicago PMI for February (Fri 0945 EST; Fri 1445

GMT)

Consensus Forecast, Index: 52.5

Consensus Range, Index: 51.0 to 52.6

Forecasters expect a slight retreat to 52.5 from a

remarkably, surprisingly strong 54.0 in January, after years of contraction.

What changed?

US Construction Spending for November (Fri 1000 EST; Fri

1500 GMT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: 0.0% to 0.1%

US Construction Spending for December (Fri 1000 EST; Fri

1500 GMT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: 0.1% to 0.3%

A moderate 0.3 percent rise is the call for December.

|