|

Easing uncertainty over rate hikes was one of the week’s themes, led by ECB President Christine Lagarde who opened the week saying the bank’s deposit rate will soon be on the climb; this was followed by Federal Reserve minutes on Wednesday which underscored the bank’s intention for two more 50-basis-point hikes and made no mention of an upsized 75-point jolt. Stock markets rallied on both Lagarde and the Fed though the latter carried a buried warning that policy could move into the “restrictive” zone depending on how the economic outlook unfolds. A similar warning, betraying the subtext of runaway inflation, was issued at mid-week by the Reserve Bank of New Zealand.

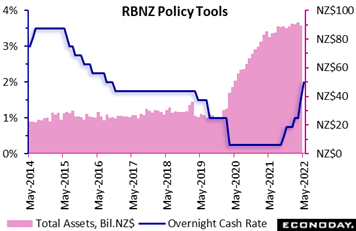

The RBNZ not only raised its policy rate by 50 basis points but, in comments echoed later Wednesday in the Fed’s minutes, also said it may raise rates above the neutral level in order to bring inflation back within its percent target range. The as-expected 50-point move to 2.0 percent is the second in a row for the RBNZ and follows 25-point moves at their three prior meetings. The bank underscored its confidence in the New Zealand economy, including the strength of the labour market, which it said gives it the scope to focus on inflation. The RBNZ is "resolute in its commitment to ensure consumer price inflation returns to within the 1.0 to 3.0 percent target range" from its current level of 6.9 percent. The RBNZ not only raised its policy rate by 50 basis points but, in comments echoed later Wednesday in the Fed’s minutes, also said it may raise rates above the neutral level in order to bring inflation back within its percent target range. The as-expected 50-point move to 2.0 percent is the second in a row for the RBNZ and follows 25-point moves at their three prior meetings. The bank underscored its confidence in the New Zealand economy, including the strength of the labour market, which it said gives it the scope to focus on inflation. The RBNZ is "resolute in its commitment to ensure consumer price inflation returns to within the 1.0 to 3.0 percent target range" from its current level of 6.9 percent.

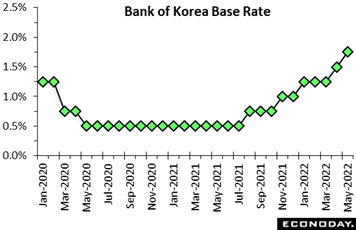

The Bank of Korea increased its main policy rate on Thursday by 25 basis points to 1.75 percent, also in line with the consensus forecast. Officials have increased this rate by 25 basis points at four of their last five meetings. Since their prior meeting last month, headline inflation increased to 4.8 percent in April, its highest level since 2011 and further above the BoK's 2.0 percent target, with core inflation picking up to 3.1 percent, its highest level since 2015. The bank said South Korea's economy "has continued to recover" despite the ongoing pandemic and the impact from the Ukraine crisis and lockdowns in major Chinese cities. Officials noted that consumer spending and labour market conditions, following the recent easing of public health restrictions, have continued to improve, but they now expect export growth to moderate. Officials expect GDP growth in 2022 will be "somewhat below" the forecast of 3.0 percent made at their last meeting in February. The Bank of Korea increased its main policy rate on Thursday by 25 basis points to 1.75 percent, also in line with the consensus forecast. Officials have increased this rate by 25 basis points at four of their last five meetings. Since their prior meeting last month, headline inflation increased to 4.8 percent in April, its highest level since 2011 and further above the BoK's 2.0 percent target, with core inflation picking up to 3.1 percent, its highest level since 2015. The bank said South Korea's economy "has continued to recover" despite the ongoing pandemic and the impact from the Ukraine crisis and lockdowns in major Chinese cities. Officials noted that consumer spending and labour market conditions, following the recent easing of public health restrictions, have continued to improve, but they now expect export growth to moderate. Officials expect GDP growth in 2022 will be "somewhat below" the forecast of 3.0 percent made at their last meeting in February.

The bank also revised its inflation outlook, and in this case upward. Officials now consider headline inflation will "remain high in the 5.0 percent range for some time" and average "at the mid-4.0 percent level for the year overall". They expect core inflation "to rise to the lower-3.0 percent level for the year overall".

The statement concludes that it is appropriate "to conduct monetary policy with more emphasis on inflation for some time, as the Korean economy is expected to continue its recovery and inflation to run above the target level for a considerable time". Officials also advised that they will "further adjust the degree of policy accommodation", indicating that further rate hikes are likely in coming months.

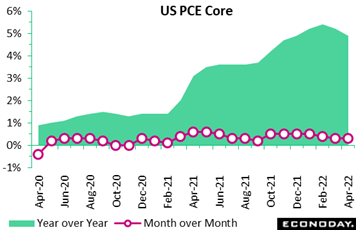

The PCE indexes in the US aren’t the latest readings, but they are the most important when it comes to the impact of inflation on US monetary policy. The overall PCE index rose an almost dormant looking 0.2 percent on the month in April, though this follows a 0.9 percent surge in March. The core index, which excludes food and energy and is less volatile, rose 0.3 percent for a second straight month. On the year, headline inflation fell 3 tenths to a 6.3 percent level that is highly elevated but a little less so than March. The core also eased 3 tenths to 4.9 percent. These are hopeful signs that recent Fed hikes are having their desired effects and that upsized hikes to 75 basis points aren’t right now in the cards. Current policy may also be keeping inflation expectations in check which, in timely data for May, eased a tenth in the University of Michigan’s year-ahead consumer measure to 5.3 percent. Note that the Fed uses, not the CPI, but the PCE indexes in its policy assessment as weighting adjustments are more frequently updated. The PCE indexes in the US aren’t the latest readings, but they are the most important when it comes to the impact of inflation on US monetary policy. The overall PCE index rose an almost dormant looking 0.2 percent on the month in April, though this follows a 0.9 percent surge in March. The core index, which excludes food and energy and is less volatile, rose 0.3 percent for a second straight month. On the year, headline inflation fell 3 tenths to a 6.3 percent level that is highly elevated but a little less so than March. The core also eased 3 tenths to 4.9 percent. These are hopeful signs that recent Fed hikes are having their desired effects and that upsized hikes to 75 basis points aren’t right now in the cards. Current policy may also be keeping inflation expectations in check which, in timely data for May, eased a tenth in the University of Michigan’s year-ahead consumer measure to 5.3 percent. Note that the Fed uses, not the CPI, but the PCE indexes in its policy assessment as weighting adjustments are more frequently updated.

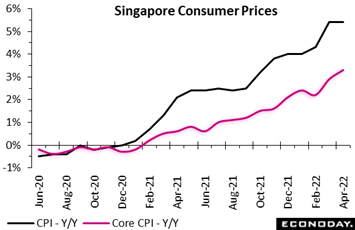

But inflation in many countries outside the US has yet to ease. Singapore's headline consumer price index held steady at 5.4 percent on the year in April but the Monetary Authority of Singapore's preferred measure of core inflation, which excludes the cost of accommodation and private road transport, increased 4 tenths to 3.3 percent. Both are the highest since 2012. The acceleration in core inflation in April was largely driven by electricity and gas prices, which rose 19.7 percent on the year, up from an increase of 17.8 percent in March. The year-over-year increase in food prices also picked up from 3.3 percent to 4.1 percent. Private transport costs rose 18.3 percent on the year after increasing 21.5 percent previously, mainly reflecting a smaller increase in car prices. But inflation in many countries outside the US has yet to ease. Singapore's headline consumer price index held steady at 5.4 percent on the year in April but the Monetary Authority of Singapore's preferred measure of core inflation, which excludes the cost of accommodation and private road transport, increased 4 tenths to 3.3 percent. Both are the highest since 2012. The acceleration in core inflation in April was largely driven by electricity and gas prices, which rose 19.7 percent on the year, up from an increase of 17.8 percent in March. The year-over-year increase in food prices also picked up from 3.3 percent to 4.1 percent. Private transport costs rose 18.3 percent on the year after increasing 21.5 percent previously, mainly reflecting a smaller increase in car prices.

April’s data will likely reinforce the concerns MAS officials have about underlying price pressures. At their semi-annual policy review last month officials tightened policy by targeting a faster appreciation of Singapore's exchange rate, citing a need to "slow the inflation momentum." With their next scheduled not meeting taking place until October, the MAS may tighten policy further with an off-schedule move if inflation momentum fails to slow.

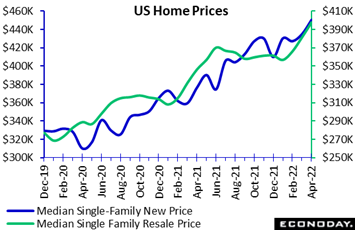

Turning back to the US, the week’s biggest news was a collapse in housing data, a collapse however that hasn’t yet slowed price momentum. Sales of new single-family homes fell 16.6 percent to a 591,000 annualized rate in April after a downward revision to 709,000 in March. Sales are the lowest since 582,000 in April 2020 during the very worst of the pandemic. The level was well below Econoday’s survey where the consensus was 750,000 and the low end of the range at 700,000. Turning back to the US, the week’s biggest news was a collapse in housing data, a collapse however that hasn’t yet slowed price momentum. Sales of new single-family homes fell 16.6 percent to a 591,000 annualized rate in April after a downward revision to 709,000 in March. Sales are the lowest since 582,000 in April 2020 during the very worst of the pandemic. The level was well below Econoday’s survey where the consensus was 750,000 and the low end of the range at 700,000.

Despite slower sales and more plentiful inventories, the latter now at a very fat 9.0 months, the median price of a new home rose, not fell, 3.6 percent to $450,600 for a year-over-year gain 19.6 percent. And resale data, posted in the prior week, told the same story, with sales falling 2.4 percent on the month while the median price, at $391,200, rose 4.4 percent for annual appreciation of 14.8 percent.

High and still rising prices as well as rising mortgage interest rates have substantially reduced home affordability, but will they slow price escalation? Very likely, but whether prices change course and move lower is another question. Other data in the week included a 3.9 percent decline for pending resales, the sixth decline in a row. The boom brought on by historic lows in mortgage rates and by changing housing needs during the pandemic is pretty much over.

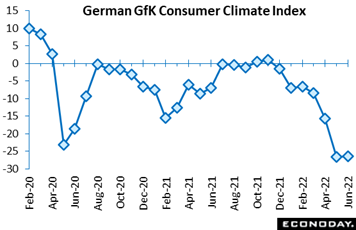

GfK confirmed steep deterioration in consumer sentiment in May but, in a positive, it also showed little change ahead for June. The climate indicator was revised down a tick to minus 26.6 in May, a drop of nearly 11 points versus April and a record low. But sentiment next month is expected to edge up to minus 26.0. Easing Covid restrictions are boosting economic expectations which climbed 7.1 points to minus 9.3. However, this is still down more than 50 points on the year and historically very weak. Income expectations similarly improved, gaining 7.6 points to minus 23.7 but this too was a sizeable 43.2 points short of its mark in May 2021. At the same time, the propensity to buy dipped a further 0.5 points to minus 11.1, warning that household consumption is likely to remain soft. While offering some hope that the deterioration in consumer morale may be over, the latest results suggest that German households are still very cautious and are unlikely to embark on any major spending sprees anytime soon. GfK confirmed steep deterioration in consumer sentiment in May but, in a positive, it also showed little change ahead for June. The climate indicator was revised down a tick to minus 26.6 in May, a drop of nearly 11 points versus April and a record low. But sentiment next month is expected to edge up to minus 26.0. Easing Covid restrictions are boosting economic expectations which climbed 7.1 points to minus 9.3. However, this is still down more than 50 points on the year and historically very weak. Income expectations similarly improved, gaining 7.6 points to minus 23.7 but this too was a sizeable 43.2 points short of its mark in May 2021. At the same time, the propensity to buy dipped a further 0.5 points to minus 11.1, warning that household consumption is likely to remain soft. While offering some hope that the deterioration in consumer morale may be over, the latest results suggest that German households are still very cautious and are unlikely to embark on any major spending sprees anytime soon.

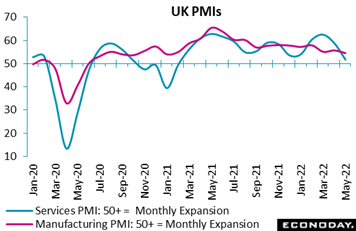

There’s plenty of action in the UK right now, and much of it is upsetting. UK business activity almost dried up in May. The flash services index tumbled more than 7 points from April's 58.9 to 51.8, a 15-month trough. Manufacturing lost momentum too but at 54.6, a 16-month low, the latest flash print was only 1.2 points below April. Growth in aggregate new business (both services and manufacturing together) slowed for a third straight month while a small increase in total backlogs masked a fall in manufacturing. Employment still expanded but by the least degree in 13 months as firms sought to reduce labour costs; business expectations deteriorated for a fourth straight month and to their weakest level in two years. There’s plenty of action in the UK right now, and much of it is upsetting. UK business activity almost dried up in May. The flash services index tumbled more than 7 points from April's 58.9 to 51.8, a 15-month trough. Manufacturing lost momentum too but at 54.6, a 16-month low, the latest flash print was only 1.2 points below April. Growth in aggregate new business (both services and manufacturing together) slowed for a third straight month while a small increase in total backlogs masked a fall in manufacturing. Employment still expanded but by the least degree in 13 months as firms sought to reduce labour costs; business expectations deteriorated for a fourth straight month and to their weakest level in two years.

Worsening sentiment in part reflects the ongoing surge in input costs which hit a new all-time peak, in no small way due to higher wage bills in services. By contrast, output price inflation actually eased slightly from April's record high as customer resistance to rising prices forced companies to accept tighter profit margins. Put simply, May’s results are surprisingly poor for an economy where the word recession is heard more and more.

President Christine Lagarde opened the week in grand style, blogging that the European Central Bank is likely to lift its deposit rate, currently at minus 0.50 percent, out of negative ground by the end of September. The deposit rate is the rate for depositing overnight money with the ECB; the bank's main policy rate, the refi rate, is currently at zero. President Joe Biden was also making headlines on Monday, repeating that he’s considering easing Trump-era tariffs on Chinese goods and warning, in the latest round of war-footing, that the US would come to the military defense of Taiwan were it to be attacked. President Christine Lagarde opened the week in grand style, blogging that the European Central Bank is likely to lift its deposit rate, currently at minus 0.50 percent, out of negative ground by the end of September. The deposit rate is the rate for depositing overnight money with the ECB; the bank's main policy rate, the refi rate, is currently at zero. President Joe Biden was also making headlines on Monday, repeating that he’s considering easing Trump-era tariffs on Chinese goods and warning, in the latest round of war-footing, that the US would come to the military defense of Taiwan were it to be attacked.

US company news erupted on Tuesday as Snap fell 43 percent after warning of slowing growth. The news sent other social media companies lower including Meta Platforms, down 8 percent, and Twitter which fell 6 percent. Chinese news was conflicted all week between government support for the economy but no letup in government lockdowns. China's state television said Tuesday the government would step up efforts to support the economy, including broadening tax rebates, postponing social security payments, cutting vehicle taxes, and launching new investment projects. Yet lockdowns in Shanghai were still in place.

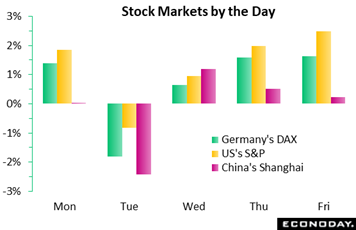

Germany's DAX had a good week, rising 3.2 percent and gaining 0.6 percent on Wednesday following the GfK survey that showed stability, however cautious, in consumer sentiment. But it was retailers, and how strong US spirits are, that are increasingly dominating market direction, beginning in the prior week with bad news from Target and following in the latest week with mostly good news, starting on Wednesday with a 14 percent gain for high-end department store chain Nordstrom which, in contrast to many retailers, raised guidance. Good news continued on Thursday with Macy’s jumping 19 percent after beating estimates as did discount chain Dollar General which rose 14 percent.

China was back in the news Friday as Premier Li Keqiang warned of possible contraction in the second quarter and offered no hint that Covid lockdowns are about to be lifted. Chinese industrial profits also didn’t help, down 8.5 percent on the year in April for the steepest decline since the beginning of the pandemic two years ago. The Shanghai ended the week with a 0.5 percent loss. But the US and Europe ended the week on the upswing as the PCE price indexes begin to show less heat, lifting the S&P which, up 6.6 percent on the week and 2.5 percent on the day, ended a 7-week losing streak. Shares in Europe had their best week since mid-March.

Canada, at plus 13 on Econoday’s consensus divergence index (ECDI), continues to outpace forecasters as it has consistently since the beginning on March. Accordingly, Bank of Canada tightening on Wednesday looks like a done deal. By contrast, the US for the past month has been missing expectations, at an ECDI of minus 24 following a sweep of collapsing housing data that highlights Federal Reserve silence on upsized rate hikes. In Europe, the Eurozone, at plus 2, has largely matched market expectations with an unexpected improvement in Germany contrasting with minor underperformance in both France and Italy. Across the Channel, following a suite of surprisingly weak data at the start of May, the UK is now outperforming expectations, at plus 14 and bolstering speculation for another Bank of England rate hike next month.

**Contributing to this article were Jeremy Hawkins, Brian Jackson, Mace News, Max Sato, and Theresa Sheehan

Central bank activity will center on the Bank of Canada which is widely expected to raise its policy rate by another 50 basis points at its Wednesday meeting. Moderation in May is the call for Germany’s CPI which, still expected to be overheated, will kick the week off on Monday. Mixed results are also expected for harmonised consumer prices from the Eurozone on Tuesday with the overall rate increasingly elevated but the core rate holding steady. A mixed performance for EC economic sentiment is expected on Monday.

China will weigh in with CFLP’s manufacturing PMI which is expected for Tuesday, followed on Wednesday by Caixan’s manufacturing PMI: both are expected to show easing rates of contraction.

Canadian GDP is expected to slow on Tuesday but still prove very strong, in data that will precede the BoC’s decision. Tuesday’s Japanese data are seen mixed: up for retail sales, down for industrial production, and steady for the unemployment rate. Improvement for the Swiss leading indicator is expected on Monday with Swiss GDP on Tuesday expected to be subdued.

US data will open with consumer confidence on Tuesday where a sizable drop back is expected, with slowing also expected for ISM manufacturing on Wednesday and ISM services on Friday. Another very solid but moderating employment report is expected on Friday with some moderation also expected for wages.

KOF Swiss Leading Indicator for May (Mon 07:00 GMT; Mon 09:00 CEST; Mon 03:00 EDT)

Consensus Forecast: 102.3

Expected to rise 6 tenths to 102.3, KOF's leading indicator rebounded in April to a stronger-than-expected 101.7 after having fallen sharply in March.

Eurozone: EC Economic Sentiment for May (Mon 09:00 GMT; Mon 11:00 CEST; Mon 05:00 EDT)

Consensus Forecast: 104.9

Consensus Forecast, Industrial Sentiment: 6.4

Consensus Forecast, Consumer Sentiment: -21.1

The Ukraine war has been pulling down economic sentiment, from 106.7 in March to 105.0 in April which was well short of expectations. A steady reading at 104.9 is expected for May. For industrial sentiment and consumer sentiment, mixed results are expected, to 6.4 from 7.9 for the former but minus 21.1 versus minus 22.0 for the latter.

German CPI, Preliminary May (Mon 12:00 GMT; Mon 14:00 CEST; Mon 08:00 EDT)

Consensus Forecast, Month over Month: 0.5%

Consensus Forecast, Year over Year: 7.5%

Consumer inflation is expected to rise 0.5 percent on the month in May for an annual rate of 7.5 percent. These would compare with April’s 0.8 and 7.4 percent, respectively.

Japanese Unemployment Rate for April (Mon 23:30 GMT; Tue 08:30 JST; Mon 19:30 EDT)

Consensus Forecast, Unemployment Rate: 2.6%

Japan's unemployment rate edged 1 tenth lower in March and is expected to hold at the 2.6 percent level in April.

Japanese Industrial Production for April (Mon 23:50 GMT; Tue 08:50 JST; Mon 19:50 EDT)

Consensus Forecast, Month over Month: -0.2%

Industrial production is expected to slip 0.2 percent in April after rising 0.3 percent in March, a month held back by a decline in auto output tied to a major earthquake in northeastern Japan. Production has missed expectations the past four reports in a row.

Japanese Retail Sales for April (Mon 23:50 GMT; Tue 08:50 JST; Mon 19:50 EDT)

Consensus Forecast, Year over Year: 2.6%

Retail sales are expected to rise 2.6 percent on the year in April after rebounding 0.9 percent in March.

China: CFLP Manufacturing PMI for May (Estimated: Tue 01:00 GMT; Tue 09:00 CEST; Mon 21:00 EDT)

Consensus Forecast: 49.3

Contraction for the CFLP manufacturing PMI is expected to ease, to 49.3 in May versus 47.4 in April which came in 1 tenth above expectations.

Swiss First-Quarter GDP (Tue 08:00 GMT; Tue 09:00 CEST; Tue 03:00 EDT)

Consensus Forecast, Quarter over Quarter: 0.4%

First-quarter GDP is expected to rise a quarterly 0.4 percent, little changed from a Covid-depressed 0.3 percent gain in the fourth quarter.

German Unemployment Rate for May (Tue 07:55 GMT; Tue 09:55 CEST; Tue 03:55 EDT)

Consensus Forecast: 5.0%

At a consensus 5.0 percent, Germany's unemployment is expected to hold unchanged for what would be a third straight month.

Eurozone HICP Flash for May (Tue 09:00 GMT; Tue 11:00 CEST; Tue 05:00 EDT)

Consensus Forecast, Year over Year: 7.7%

Narrow Core

Consensus Forecast, Year over Year: 3.5%

The flash headline annual rate for May is seen rising 2 tenths to 7.7 percent; the narrow core rate is expected to hold steady at 3.5 percent. The former came in at expectations in April and the latter above expectations.

Canadian First-Quarter GDP (Tue 12:30 GMT; Tue 08:30 EDT)

Consensus Forecast, Annualized: 5.2%

A 5.2 percent annualized growth rate is the consensus for Canadian first-quarter GDP versus 6.7 percent expansion in the fourth quarter.

US Consumer Confidence Index for May (Tue 14:00 GMT; Tue 10:00 EDT)

Consensus Forecast: 104.0

The consumer confidence index has been steady, coming in at 107.3 and 107.6 the past two reports with a downdraft to 104.0 the expectation for May.

China: Caixan Manufacturing PMI for May (Wed 01:45 GMT; Wed 09:45 CST; Tue 21:45 EDT)

Consensus Forecast: 48.0

Caixan's manufacturing PMI has missed, and sizably so, expectations the past two reports. After 46.0 in April, the consensus for May is noticeable improvement to 48.0.

Eurozone Unemployment Rate for April (Wed 09:00 GMT; Wed 11:00 CEST; Wed 05:00 EDT)

Consensus Forecast: 6.7%

Consensus for April's unemployment rate is a 1 tenth dip to 6.7 percent.

Bank of Canada Announcement (Wed 14:00 GMT; Wed 10:00 EDT)

Consensus Forecast, Change: 50 basis points

Consensus Forecast, Level: 1.50%

After raising its policy rate by 50 basis points at its April meeting to 1.00 percent, the Bank of Canada is expected to raise it by another 50 points at its June meeting.

US: ISM Manufacturing Index for May (Wed 14:00 GMT; Wed 10:00 EDT)

Consensus Forecast: 54.5

The ISM manufacturing index is expected to slow further in May to 54.5 after April's 1.7-point decline to 55.4 that missed Econoday's consensus range.

US JOLTS: Job Openings for April (Wed 14:00 GMT; Wed 10:00 EDT)

Consensus Forecast: 11.400 million

Openings, at 11.549 million in March, have exceeded expectations the past four reports. April's expectations are a step back to 11.400 million.

Eurozone PPI for April (Thu 09:00 GMT; Thu 11:00 CEST; Thu 05:00 EDT)

Consensus Forecast, Month over Month: 2.3%

Consensus Forecast, Year over Year: 38.6%

In March, producer prices came in even more overheated than expected, surging 5.3 percent on the month and 36.8 percent on the year. Another set of superheated results are expected for April, at respective rates of 2.3 and 38.6 percent.

ADP, US Private Payrolls for May (Thu 12:15 GMT; Thu 08:15 EDT)

Consensus Forecast: 240,000

Consensus Range: 200,000 to 330,000

The consensus forecast for ADP's May estimate is private payroll growth of 240,000. Looking back at April, ADP's estimate for slowing growth of 247,000 in private payrolls compared with steady growth of 406,000 in the government's data.

US Employment Situation for May (Fri 12:30 GMT; Fri 08:30 EDT)

Consensus Forecast: Change in Nonfarm Payrolls: 325,000

Consensus Forecast: Average Hourly Earnings M/M: 0.4%

Consensus Forecast: Average Hourly Earnings Y/Y: 5.3%

A 325,000 rise is Econoday's consensus for nonfarm payroll growth in May which would compare with 428,000 in both April and March. Average hourly earnings are expected to rise 0.4 percent on the month versus a 0.3 percent rise in April. This annual rate is expected to slow to 5.3 percent from 5.5 and 5.6 percent in the two prior months.

US: ISM Services Index for May (Fri 14:00 GMT; Fri 10:00 EDT)

Consensus Forecast: 56.3

The ISM services has been holding in the high 50s all year, at 57.1 in April with some moderation to 56.3 expected for May.

|